Loading articles...

Related articles

The Strait of Hormuz closure removed 20% of global seaborne oil. The Supreme Court struck down IEEPA tariffs. Golden Pass LNG fired its first train. Port Houston posted record January volumes. This briefing covers the commodity trade flows, crude import shifts, LNG/NGL export surges, petrochemical margin dynamics, and midstream investment reshaping the Houston Ship Channel corridor in real time.

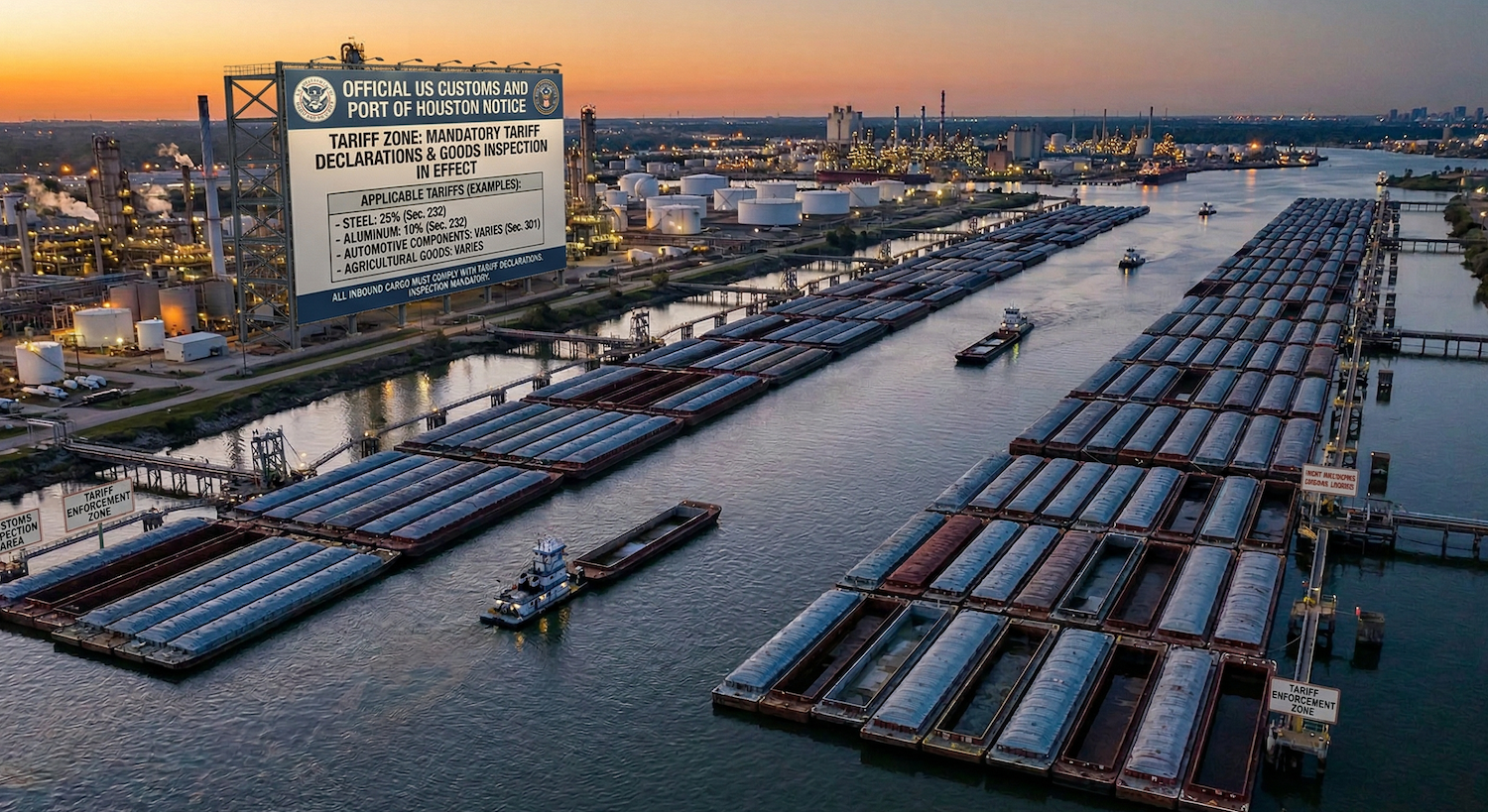

The Houston Ship Channel is navigating the most volatile commodity trade environment in decades. A Supreme Court ruling struck down IEEPA tariffs on February 20, the Strait of Hormuz effectively closed on March 4 after U.S.-Israeli strikes on Iran, and Golden Pass LNG fired its first train on March 30 — all within six weeks. For terminal operators, commodity traders, and industrial investors along the Channel, these concurrent shocks are rewriting the playbook on trade flows, margins, and infrastructure value.

Yet Port Houston posted record January container volumes and record 2025 tonnage, while midstream operators reported blowout Q4 earnings. The Channel's export-heavy commodity mix is proving remarkably resilient — and in some cases, directly benefiting from global disruption.

On February 28, 2026, the United States and Israel launched coordinated airstrikes on Iran. Iran retaliated by closing the Strait of Hormuz to commercial shipping — removing roughly 20% of global seaborne oil supply and a comparable share of LNG trade from the market. QatarEnergy declared force majeure on all LNG shipments on March 4. By mid-March, over 150 tankers sat anchored outside the strait, and 21 confirmed attacks on merchant vessels had been recorded.

The impact on global commodity prices was immediate. Brent crude surged past $100 per barrel on March 8 — the first time in four years — and peaked near $126 per barrel. Asian LNG spot prices jumped almost 39%, European wholesale gas prices more than doubled, and diesel and jet fuel prices at times topped $200 per barrel in Asian markets. The Dallas Federal Reserve modeled the closure's impact at $98 WTI and a 2.9 percentage point reduction in global GDP growth for Q2 2026.

For the Houston Ship Channel specifically, the crisis produced a paradox: feedstock costs rose, but the export premium for U.S.-produced energy widened dramatically. Gulf Coast refinery utilization surged to 96.7% in the week of March 20 — up sharply from the mid-80% range just weeks earlier — as global product shortages incentivized maximum domestic throughput.

VLCC spot freight rates exploded to over $150,000 per day on Middle East-to-Asia routes, the highest since the 2020 oil price war. More critically for Houston, the crisis redirected VLCC availability toward Atlantic basin loading ports. U.S. Gulf-to-China routes commanded rates approaching $100,000 per day, though rates subsequently eased as more vessels shifted to U.S. Gulf, Nigerian, Brazilian, and Guyanese loading.

The U.S. military campaign to reopen the strait remains ongoing. As of early April, Iran is seeking to monetize its leverage by establishing a tolling system for approved vessels, with reports of at least two ships paying roughly $2 million each for passage.

On February 20, the Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act does not authorize the president to impose tariffs. The ruling invalidated all IEEPA-based tariffs — including reciprocal tariffs and fentanyl-related duties on China, Canada, and Mexico — which by January 2026 had accounted for over 50% of all U.S. customs duties collected, or roughly $165 billion cumulative since inception.

Within hours, Trump invoked Section 122 of the Trade Act of 1974 to impose a 10% global tariff effective February 24, capped at 15% and limited to 150 days. Critically for the energy sector, energy products, critical minerals, pharmaceuticals, and USMCA-qualifying goods remain exempt. This exemption has shielded Gulf Coast refiners from the worst tariff impacts — U.S. refiners import nearly half of their 8 million barrels per day of crude oil from Canada and Mexico.

For petrochemical exporters, the picture is more complicated. The U.S. chemical industry posts a trade surplus exceeding $30 billion annually. The American Chemistry Council has acknowledged aggressive dumping from China's overcapacity while cautioning that blanket tariffs may create more economic harm than necessary. The White House excluded many major chemicals — polyethylene, polypropylene, PET, and phenols — from tariff duties, though the 150-day statutory limit on Section 122 tariffs keeps long-term planning difficult.

Port Houston handled 370,034 TEUs in January 2026 — the largest January on record, up 4% year-over-year — while many U.S. ports reported declines. Loaded imports and loaded exports each rose 5%. For the full year 2025, the port moved a record 54.5 million short tons across its public terminals and a record 4.3 million TEUs, with loaded exports up 7%.

The divergence is structural. Port Houston handles approximately 60% of all U.S. resin exports, and petrochemical products continue to anchor outbound container volumes. While China-origin container imports at U.S. ports fell 22.7% year-over-year in January 2026, Houston's export-oriented cargo mix insulated it from the import-side weakness.

February 2026 data showed continued momentum: total tonnage up 4% year-over-year, with dry bulk up 28% and liquid bulk up 31%, though steel imports remained weak — down 27% year-to-date reflecting reduced drilling activity. The Port Commission also approved a marine construction permit for ExxonMobil to build new petrochemical export loading infrastructure on the Channel.

Port Houston's FY2026 budget of $1.34 billion — the largest in its history — includes $875 million in capital spending, with $395 million for container facilities, $290 million for channel infrastructure, and $111 million for general cargo and multipurpose terminals.

The crude import mix at Gulf Coast terminals is undergoing a structural realignment. Mexico's crude exports to the United States hit a 35-year low of 503,000 barrels per day in December 2025, with Maya grade exports plunging to just 253,000 barrels per day — an 86% decline from 2020 levels. The Sheinbaum administration's push for domestic refining self-sufficiency, anchored by the Dos Bocas refinery reaching 77.5% utilization by December, is permanently redirecting barrels away from Gulf Coast refiners.

Venezuelan crude has surged to partially fill the gap. Following geopolitical changes in early January 2026, total Venezuelan exports to the United States nearly tripled to 284,000 barrels per day in January. Vitol and Trafigura received U.S. licenses to market Venezuelan oil alongside Chevron. S&P Global estimated Gulf Coast refiners could absorb an additional 300,000–400,000 barrels per day of heavy Venezuelan crude to restore coking utilization to 2024 levels.

Canadian heavy crude deliveries to the Gulf Coast fell to roughly 700,000 barrels per day in 2025 — down over 100,000 barrels per day from the 2024 peak — as the Trans Mountain Expansion pipeline diverted barrels to Pacific markets. Approximately two-thirds of TMX exports now flow to Asia-Pacific, with China becoming the second-largest destination for Canadian crude.

Golden Pass LNG's March 30 first production from Train 1 at Sabine Pass could not have been better timed. The 6 million ton-per-annum unit started producing LNG just weeks after Iranian missile strikes damaged Qatar's Ras Laffan complex — home to roughly 20% of global LNG supply. First export cargoes are expected in Q2 2026.

U.S. LNG export capacity stood at approximately 17 Bcf/d at year-end 2025 and is on track to exceed 19 Bcf/d by year-end 2026, with Cheniere's Corpus Christi Stage 3 adding three more trains through fall 2026. The EIA forecasts U.S. LNG gross exports increasing 15% to 16.4 Bcf/d in 2026. An estimated 18–20 Bcf/d of new pipeline capacity is being built along the Gulf Coast, including Kinder Morgan's $1.8 billion Trident Pipeline (2.0 Bcf/d, broke ground January 2026) and the Blackcomb Pipeline (2.5 Bcf/d, second half of 2026).

On the NGL side, Enterprise Products is expanding its Houston Ship Channel export terminal, adding approximately 300,000 barrels per day of propane and butane export capacity for a total of 1.135 million barrels per day by end of 2026. Enterprise loaded between 350 and 360 million barrels of NGLs across 744 ships in 2025. Targa Resources reported record loadings at its Galena Park Marine Terminal, averaging 14 million barrels per month in Q4 2025, with an expansion to 19 million barrels per month targeted for Q3 2027.

Before the Iran conflict, the petrochemical sector was enduring its worst margin environment in decades. North American polyethylene chain margins averaged $580 per metric ton, far below the historical average of $830. The American Chemistry Council reported U.S. chemical exports fell 2.0% in 2025, with plastic resin exports declining 7.5% year-over-year in January 2026.

Chinese capacity expansion remains the structural headwind. China's PE production capacity is growing at a projected 27% expansion rate in 2026. Brazil imposed antidumping duties of $199 per ton on U.S. polyethylene, with preliminary findings suggesting duties could nearly triple, potentially redirecting more than 9% of U.S. PE exports.

Then the Hormuz closure upended everything. Ethylene costs on the Houston Ship Channel rose 66% following the onset of hostilities. Asian polyethylene prices jumped 40–50% as variable production costs in Asia doubled. Some 8 million tons per year of ethylene glycol exports from the Middle East were effectively taken offline. Every company capable of producing at maximum is doing so — the war upended all of the petrochemical industry's expectations for 2026.

Dow announced 4,500 job cuts globally as part of its Transform to Outperform restructuring, while simultaneously noting encouraging signs from ethylene capacity rationalization and the elimination of Chinese VAT export rebates.

Enterprise Products Partners reported record Q4 EBITDA of $2.7 billion, with NGL pipeline volumes hitting a record 4.9 million barrels per day and gas processing inlets reaching a record 8.1 Bcf/d. Full-year distributable cash flow was $7.9 billion. Enterprise's 65-acre waterfront acquisition adjacent to its EHT facility will add at least two Suezmax-capable deepwater docks to a complex already comprising 18 ship docks and access to approximately 125 pipelines and 400 million barrels of storage.

Kinder Morgan reported Q4 adjusted EBITDA of $2.271 billion, up 10% year-over-year, earning an S&P credit upgrade to BBB+ in January. The company's $8.1 billion project backlog is 89% natural gas-focused, and it delivers over 40% of natural gas feeding U.S. LNG export facilities.

Kirby Corporation posted record full-year EPS of $6.33 with marine transportation operating margins reaching the low-20% range. CEO David Grzebinski noted Venezuelan crude re-entry and tariff developments could present upside for barge demand.

Cando Rail & Terminals closed its acquisition of Texas Deepwater Partners' rail terminal on December 4, 2025, renaming it Cando Channelview Terminal — a 900-railcar facility on the north side of the Ship Channel serving major petrochemical producers.

The near-term outlook hinges entirely on the Hormuz crisis duration. The EIA's March STEO forecasts Brent averaging $91 per barrel in Q2 2026, falling to $70 by Q4 if flows resume. The IEA authorized its largest-ever emergency reserve release of 400 million barrels on March 11, and the Trump administration issued a 60-day Jones Act waiver on March 17 to allow foreign-flagged vessels to carry fuel between U.S. ports — an unprecedented measure.

The Greater Houston Partnership forecasts 30,900 new jobs in metro Houston in 2026, with the metro economy reaching $758 billion in GDP — surpassing three-quarters of a trillion dollars for the first time. Houston's manufacturing output of $126.9 billion in 2024 ranked first nationally for the third consecutive year.

The Golden Triangle Polymers facility — the $8.5 billion CPChem/QatarEnergy joint venture in Orange, Texas — is targeting startup in the second half of 2026 with the world's largest ethane cracker (2,080 KTA) and two HDPE units (2,000 KTA combined), with nearly all new production aimed at export markets. Trump announced a $300 billion deal for the first new greenfield U.S. refinery since 1976 at Port of Brownsville, with groundbreaking planned for Q2 2026.

The Channel's structural advantages — ethane cost advantage, deepening waterway, expanding export infrastructure, and proximity to the world's largest refining and petrochemical complex — are being stress-tested by simultaneous tariff upheaval and the most severe global energy supply disruption since the 1970s. So far, the infrastructure is not just holding up — it's proving more strategically valuable than ever.

Ameritank's 147-acre La Porte facility sits at the center of this corridor with direct Houston Ship Channel frontage, a deepwater barge dock, 840 MW of power capacity, Union Pacific rail, and 4 billion gallons of annual water access — infrastructure purpose-built for the commodity flows reshaping global energy trade. Connect with the Ameritank team.

Andrew Viera

Business Development Executive, Ameritank

Andrew manages offtaker relationships, capital partnerships, and strategic positioning for Ameritank's 147-acre terminal on the Houston Ship Channel. He works across terminal development, investor relations, and market analysis to connect infrastructure capacity with commodity demand across the Gulf Coast energy corridor.