Loading articles...

Related articles

Brookfield just paid $1.2 billion for Peakstone's IOS portfolio. Alterra raised $925M. JPMorgan and Zenith built a $1.5B joint venture. The Industrial Outdoor Storage asset class hit $214 billion — and every major U.S. metro except Houston has made it functionally illegal to build new supply. Inside why La Porte, Pasadena, and Baytown are the most asymmetric IOS play in the country, with national port volumes, a petrochemical buildout, and the only major-metro zoning environment where new IOS can still be developed.

In February 2026, Brookfield Asset Management agreed to pay $1.2 billion in cash to take Peakstone Realty Trust private — a 34% premium that valued the REIT at $21 per share. The deal added 76 properties to Brookfield's portfolio: 60 of them are Industrial Outdoor Storage (IOS) yards, the asset class most institutional investors had never heard of three years ago.

The Brookfield-Peakstone deal is now the largest pure IOS transaction in history. It will not be the largest for long.

Behind it sits a wave of institutional capital that has redefined an entire corner of commercial real estate in under five years. Alterra IOS, the nation's largest IOS owner, closed its $925 million Venture III fund in May 2024, surpassing both its $750 million target and its $850 million hard cap. Zenith IOS scaled its J.P. Morgan joint venture from $700 million in 2022 to over $1.5 billion in gross asset value today. JPMorgan's own real estate income trust paid $95.2 million for a 16-property IOS portfolio in mid-2025. Realterm bought 13 properties from Brookfield for $277 million in January 2025. According to CRE Daily, institutional investors deployed more than $900 million into IOS in 2025 alone — and Fident Capital documented over $3 billion raised in a single Q1 2025 window by funds including TPG Angelo Gordon, JPMorgan, and several state pensions.

This is what an institutional asset class formation looks like in real time.

But here is what almost none of the coverage has noticed: every other major IOS market in America has just made it functionally illegal to build new supply. The Inland Empire passed AB 98 in September 2024, mandating new warehouse alignment with truck routes by January 2026 and triggering moratoriums in six Southern California cities. Los Angeles County is rewriting its zoning code to outlaw outdoor cargo container storage in entire industrial districts. Atlanta's "ATL Zoning 2.0" rewrite takes effect in January 2026. Maricopa County passed a Modernized Zoning Ordinance tightening industrial standards across Phoenix.

The result is a paradox: $214 billion in addressable market, $3 billion in fresh institutional capital, 2.5% national vacancy — and a supply curve frozen in place across virtually every major metro.

Except one.

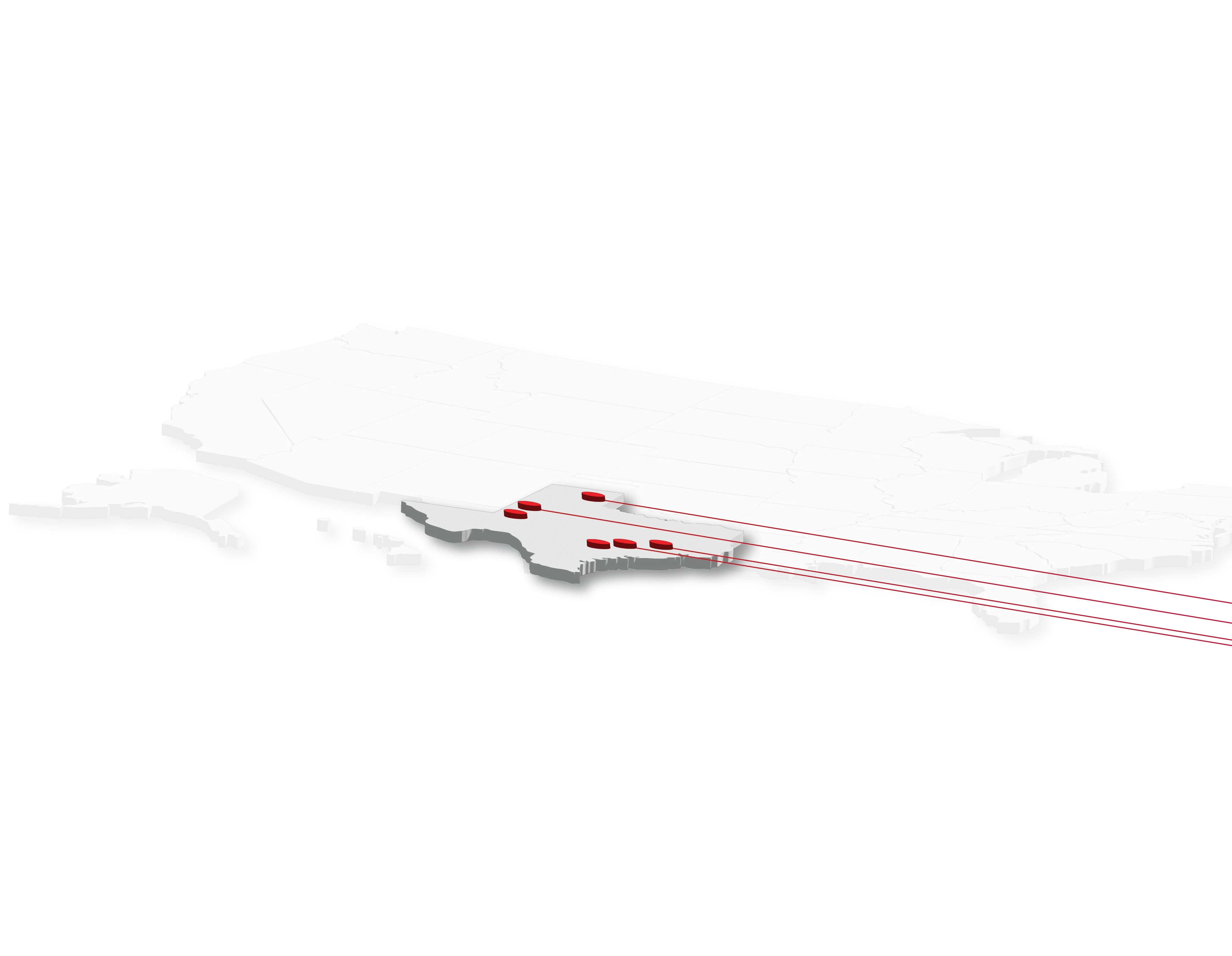

Houston is the only major U.S. city without a zoning code. The municipalities along the Houston Ship Channel — La Porte, Pasadena, Baytown, Channelview — all operate under deed restrictions and platting rather than parcel-by-parcel zoning. The Texas legislature went further in 2025, preempting local restrictions on industrial uses in several categories. While every other top-10 IOS market is layering new restrictions, Houston is the structural exception — the rare metro where the demand is national-tier and the supply curve is still elastic.

This is why Brookfield, JPMorgan, Alterra, Zenith, Triten, Apricus, Stonemont, Dalfen, and a half dozen other institutional buyers are racing to La Porte first. This is the asymmetric IOS play.

Before unpacking the Houston opportunity, it helps to define the asset class. Industrial Outdoor Storage refers to fenced, paved or gravel yards used to store equipment, vehicles, containers, materials, or inventory outside — usually with minimal vertical improvements. A typical IOS site has a perimeter security fence, lighting, surface treatment, some access control infrastructure, and often a small office or guard shack. There is no roof. There are no docks. There is no HVAC.

The tenants tend to fall into two categories. CBRE divides them into transport/logistics/fleet operators — cross-dock truck terminals, container storage operators, trailer parking, fleet maintenance yards — and equipment/bulk storage users — contractor yards, building materials suppliers, car rental fleets, landscaping companies, and equipment rental operators. Increasingly, the tenant base also includes utilities, public-sector contractors, oil and gas service companies, and renewable energy operators staging panels and batteries.

The economics of IOS are structurally different from a Class A warehouse. There is no roof to replace every 20 years at $5 to $10 per square foot. There is no sprinkler system. There are no dock levelers. The capital expenditure reserve required to keep an IOS yard operating is a small fraction of what a warehouse needs. Transwestern characterizes IOS as a "low-improvement, low-capex, high-NOI-margin" asset class, and that description is precisely why institutional capital has rushed in.

The performance numbers explain the rush better than any pitch deck. In Q4 2025, CBRE measured national IOS vacancy at 2.5%, compared to 6.47% for traditional industrial. IOS rents averaged $13.10 per square foot, a 17.9% premium over traditional industrial at $10.85. CRE Daily reported IOS rents have grown 123% since 2020, with a five-year average rent growth above 8.8% — the highest of any industrial subsector.

Compared to traditional warehouse rent growth in the low single digits, IOS is doing what self-storage did fifteen years ago: transitioning from an "alternative" asset class into core institutional real estate. NAIOP describes the shift as "the institutionalization of industrial outdoor storage," and Hamilton Lane has documented IOS as a fully formed allocation category for institutional real estate portfolios.

The clearest signal of institutional commitment is fund size. In May 2024, Alterra Property Group's IOS Venture III closed at $925 million, filling its allocation in eight months versus the industry-average 24. The fund's predecessor, Alterra IOS Venture II, had raised $524 million. Behind both funds sits a roster of public and private pensions, university endowments, sovereign wealth funds, asset managers, and family offices.

Alterra's debt stack is just as telling. In October 2025, Blue Owl Capital committed a $150 million loan facility to Alterra IOS. Blackstone Mortgage Trust followed with a $189 million commitment. And in February 2026, Alterra IOS announced a passive minority investment from Almanac, the private real estate arm of Neuberger Berman — the kind of structural validation that tells the rest of Wall Street that Alterra is no longer a niche operator.

By Q4 2025, Alterra had assembled a portfolio of 400-plus properties across 38 states. Their February 2026 acquisition of a national truck terminal portfolio from R+L Carriers added another 10 properties, 45 usable acres, 445 drive-in doors, and over 238,000 square feet of warehouse space for $49.5 million. Nine of the ten properties were leased back to multinational freight carriers on day one.

Alterra is not alone. Zenith IOS launched its $700 million joint venture with J.P. Morgan Asset Management in February 2022 and has since scaled the platform to over $1.5 billion in gross asset value. In March 2025, Zenith refinanced 30 of its IOS assets through a $120 million loan pool arranged through Cooper-Horowitz with Washington Capital Management. The same year, Zenith acquired an 11-property portfolio in Greater Phoenix. According to Zenith's own 2025 disclosures, the company signed more than 3.5 million square feet of leases across 10 markets last year alone.

JPMorgan is not just backing Zenith. JPMREIT — the firm's flagship real estate income trust — paid $95.2 million for a 16-property IOS portfolio in mid-2025, expanding directly into IOS as a core holding. Realterm and J.P. Morgan have also formed a joint venture that acquired a seven-property national IOS portfolio. And in November 2024, Alterra and J.P. Morgan jointly sold a 51-property IOS portfolio for $490 million.

Industrial Outdoor Ventures recapitalized through a joint venture with Stockbridge and now plans to acquire $100 to $200 million per year. The platform owns 80-plus assets across 18 markets, encompassing more than 1,000 acres of yard and 2.4 million square feet of buildings. Triten Real Estate Partners runs a programmatic joint venture targeting $500 million in 16 markets and has averaged 18 acquisitions per year since 2020.

Then there is the Brookfield deal. In February 2026, Brookfield Asset Management agreed to take Peakstone Realty Trust private for $1.2 billion. The transaction included 76 properties — 60 of them IOS — and represented the single largest pure IOS deal in the history of the asset class. The deal will close in Q2 2026 after a 30-day go-shop period. CoStar called it "Brookfield's biggest industrial bet of 2026."

Add it all up. Per Fident Capital, the addressable IOS market in the U.S. is roughly $200 to $214 billion across more than 75,000 properties. Institutional investors raised $1.7 billion in 2024 alone. They raised more than $3 billion in a single Q1 2025 window. And the largest single deal in the asset class's history happened seven weeks ago.

For perspective, Bisnow originally sized the IOS opportunity at $200 billion, describing it as "you've driven past them a million times." Two years later, Bisnow's headline reads "IOS is 'Surprisingly Resilient.' Institutions Want In." Yet the supply that institutional capital is chasing is shrinking, not growing.

The institutional thesis on IOS rests on a single assumption: supply is structurally constrained because zoning is structurally hostile. That assumption is being validated in real time across virtually every major metro outside Houston.

In September 2024, California Governor Gavin Newsom signed Assembly Bill 98 (AB 98), the Inland Empire's most aggressive warehouse and industrial restriction in a generation. The bill mandates that new warehouses align with designated truck routes by January 1, 2026, in twelve "Warehouse Concentration Region" jurisdictions: Chino, Colton, Fontana, Jurupa Valley, Moreno Valley, Ontario, Perris, Rancho Cucamonga, Redlands, Rialto, Riverside, and San Bernardino. AB 98 also bans heavy-duty diesel truck traffic next to homes, schools, parks, and nursing homes; mandates minimum setback distances; and requires landscaped buffers around new industrial development. According to the Inland Empire Community News, six of those cities introduced local moratoriums after AB 98 took effect.

Los Angeles County followed with its own zoning rewrite. According to Allen Matkins' 2024 Land Use and Environmental Update, LA County's updated zoning code will outlaw outdoor storage of cargo containers and commercial vehicles in designated areas, replacing legacy industrial designations with hybrid "Industrial Transition Areas" intended to phase industrial uses out near residential neighborhoods.

Atlanta is rewriting its zoning code from scratch. The "ATL Zoning 2.0" project — the city's first comprehensive code update since 1982 — targets adoption in January 2026 and replaces legacy industrial designations entirely. The Atlanta Regional Commission published a Truck Parking Zoning and Guidance document in December 2024, which serves as a model ordinance for member jurisdictions and explicitly recommends restrictions on outdoor truck parking near residential areas.

The cumulative effect of these zoning moves is dramatic. According to Commercial Property Executive's Q4 2025 IOS coverage, "no one's giving zoning variances for IOS real estate." FreightWaves' coverage of the broader 'NIMBY' trend noted that "it's harder to build warehouses today than 15 years ago. No sector has been so directly and persistently targeted." And Partners Real Estate's Texas IOS Report measures California IOS entry costs at up to $2.4 million per acre in premium zones, including site improvements.

For institutional buyers underwriting an asset class on the basis of supply scarcity, this is the validation thesis. Every restriction that passes makes the existing inventory more valuable. Every variance denied compresses the cap rate spread by another basis point. But every restriction also makes the question more urgent: where do you actually deploy the capital?

Houston is the only major U.S. city without a formal zoning code. HAR.com's Houston land use guide describes the city's regulatory environment as governed by deed restrictions, platting, and use regulations rather than parcel-by-parcel zoning. The City of Houston's own Planning and Development Department confirms the absence of a formal zoning code, noting that development standards are enforced through subdivision and infrastructure ordinances rather than zoning districts.

This is not a small distinction. In Inland Empire, an IOS developer needs a use permit, an environmental review, a community plan amendment, and increasingly a moratorium waiver. In Houston, the same developer needs to confirm deed restrictions, file a plat, and meet infrastructure standards. The entitlement risk is dramatically lower. The timeline is dramatically shorter. The political opposition is dramatically smaller.

Pasadena, La Porte, and Baytown — the three municipalities that anchor the petrochemical corridor along the Houston Ship Channel — all operate under similar deed-restriction regimes. Pasadena's planning page confirms the city has no traditional zoning. La Porte and Baytown follow the same model. The legal complexity that makes IOS development functionally impossible in California is simply not present in Texas, and especially not in the Ship Channel corridor.

The Texas legislature reinforced this advantage in 2025. According to the Fort Worth Report, the legislature preempted local restrictions on certain categories of industrial uses, further insulating industrial development from municipal pushback. The political environment in Texas remains structurally pro-development, and pro-industrial-development specifically.

There are limits. Austin and San Antonio along the I-35 corridor face IOS-restrictive municipal zoning. Partners Real Estate's Texas IOS Report notes that Texas is not uniformly friendly to IOS — but Houston is the major-metro outlier within Texas, and the Houston Ship Channel is the most permissive submarket within Houston. This is why every institutional IOS aggregator has Houston in their top three target markets.

If Houston had only the supply elasticity story, it would be an interesting market. What makes it the most asymmetric IOS play in the country is that the demand drivers are also national-tier — and accelerating.

Start with the port itself. According to Port Houston's January 2026 announcement, 2025 was the most successful year in port history. Container throughput hit 4,303,345 TEUs, up 4% year over year. Loaded exports rose 7%. Total cargo handled hit 54,491,066 short tons, up 3%. Port Houston crossed the three million TEU mark in September 2025 — the fastest pace in the port's history.

The port handles roughly 60% of all U.S. resin exports. It is the largest petrochemical complex in the United States, with Colliers estimating roughly 400 petrochemical facilities in the corridor. The Bayport Container Terminal, post-Project 11, can now handle vessels in the 15,000 to 17,000 TEU range — equivalent to Panama Canal-sized ships. Wharf 7 at Bayport added 1,000 feet of berth in late 2025. Five new RTGs were delivered in 2025, with another six arriving in March 2026.

Behind the port sits the petrochemical buildout. ExxonMobil announced its Baytown Refinery Reconfiguration Project in 2025, with construction underway in early 2026 and startup targeted for 2028. The project will require 700-plus contractor jobs at peak construction. ExxonMobil also has a $2 billion Baytown chemical expansion under construction. Enterprise Products Partners is expanding NGL export capacity by 300,000 barrels per day at the Enterprise Hydrocarbons Terminal, with service expected to start by the end of 2026.

These projects do not just create permanent jobs. They create staging requirements. Construction laydown yards. Pipe storage. Trailer parking for contractor fleets. Heavy equipment yards. Frac sand and proppant staging. Container storage for project cargo. Each major petrochemical announcement on the Ship Channel translates almost directly into IOS demand within a 10-mile radius.

The manufacturing share of Houston industrial tenants reflects this shift. According to Newmark and Bisnow's December 2025 coverage, the manufacturing share of industrial tenants in Houston jumped from 10% to 30% over the past several years, driven by onshoring and petrochemical expansion. Stonemont Financial acquired a 5.8-acre IOS facility at the entrance to Port Houston's Barbours Cut terminal in La Porte. Apricus Realty Capital acquired a 9.2-acre IOS facility in Channelview, fully leased to GFL Plant Services for petrochemical operations.

Then there is the Permian connection. The Permian Basin is the single largest consumer of frac sand in the United States, and a significant share of that sand and the related oilfield service equipment moves through the Houston Ship Channel corridor. World Oil reported in January 2026 on continued expansion of dry frac sand capacity in West Texas. The economic geometry — Permian to Houston to export — keeps frac sand staging, pipe yards, and oilfield equipment laydown as a permanent IOS demand category along the Ship Channel.

The cumulative effect is a demand profile that compares favorably to any IOS market in the country. Same record port volumes as Long Beach. Same petrochemical anchors as Louisiana's chemical corridor. Same trucking density as Dallas-Fort Worth. Same energy services tailwinds as Permian basin gateways. And Houston has all of them at once.

If institutional capital needs one more validation that IOS demand is non-discretionary, the answer is the truck parking shortage.

According to the American Transportation Research Institute, the United States has roughly one truck parking space for every 11 truck drivers. The total inventory is approximately 313,000 spaces nationally — about 40,000 at public rest areas and 273,000 at private truck stops. The average rest area has 19 truck parking spaces. The Northeast averages 15. Drivers spend 56 minutes per day searching for parking, costing the average driver $4,600 per year in lost wages and 9,300 lost revenue-earning miles.

Truck parking ranks #2 on ATRI's 2025 Top Critical Issues survey, behind only the broader economy. It has been in the top three for three consecutive years.

The shortage is not solvable by drivers being more efficient. It is structural. The Federal Motor Carrier Safety Administration's Hours of Service rules cap driving at 11 hours within a 14-hour on-duty window, followed by 10 hours of mandatory off-duty time. Drivers must take a 30-minute break within the first 8 hours on duty. The HOS clock does not pause for missing parking. Drivers must stop legally regardless of where they are. Combined with the 1-space-per-11-drivers shortfall, this forces fleet operators to lease dedicated parking yards — which is to say, IOS — to guarantee their drivers can stop legally each night.

Texas has been ahead of most states on the supply response. According to TxDOT's Texas Freight Advisory Committee September 2025 meeting summary, Texas has grown statewide truck parking capacity by approximately 34% — from roughly 26,000 spaces to over 35,000 — in two years. TxDOT also developed a Houston/Southeast Texas Truck Parking Action Plan in 2024 specifically for the Houston and Beaumont districts. Even with that progress, the shortage remains acute.

For IOS operators along the Houston Ship Channel, the truck parking crisis is the single most reliable demand signal in the asset class. Fleets do not lease dedicated yards because they want to. They lease them because the alternative is illegal driving and DOT violations. The demand is regulatory, not aspirational, and that is precisely why institutional buyers consider it durable through any economic cycle.

Demand is one side of the equation. Supply is the other. And the supply story along the Houston Ship Channel is starker than most institutional buyers realize.

In its definitive coverage of the corridor, Bisnow Houston reported that only five large industrial tracts remain in the Houston Ship Channel area. Future development is shifting northeast into Chambers County, where land is still available but lacks the immediate Ship Channel access that defines the established corridor. The southeast Houston submarket — anchored by Highway 146, Highway 225, Beltway 8, I-10, and I-45 — is the metro's top-performing industrial submarket and the most constrained.

Per Partners Real Estate's Q1 2025 Houston Industrial Quarterly Report, Houston added more than 83 million square feet of warehouse since 2020 and absorbed 12.6 million square feet in 2025 alone. The Q4 2025 industrial NNN rent in Houston averaged $0.89 per square foot per month — a 13.8% jump from $0.78 the previous year. Newmark measured Houston IOS vacancy at 3.4%, versus 7.4% for traditional Houston industrial in Q4 2025. The IOS vacancy gap in Houston tracks the national pattern almost exactly.

The pace of recent IOS transactions in the corridor confirms how aggressively institutional buyers are moving. In September 2024, Alterra IOS acquired four Houston-area sites totaling 17 acres, including two adjacent properties at 8121 and 8223 Parkside Avenue in Baytown's Bay 10 Business Park (7.2 acres plus a 50,000 square foot warehouse), 5100 Underwood Road in Pasadena, and 9002 Wayfarer Lane in Houston. The deal was funded through Alterra IOS Venture III. Triten Real Estate Partners closed a 25-acre Houston portfolio sale including 12202 Cutten Road in northwest Houston (20.1 acres) and 1503 Industrial Drive in Missouri City (5.45 acres plus a tilt-wall building). Partners Real Estate brokered the sale of a 50,532 square foot facility on 44.6 acres in Katy and a 31,540 square foot facility on 6.30 acres at 11049 Eastex Freeway in north Houston.

Per-acre pricing in Houston still runs 60% to 80% below coastal IOS markets. IOS YardDogs and IOS List have documented per-acre pricing ranging from $400,000 to $700,000 in Fort Worth, $700,000 to $1.5 million in Salt Lake City, and $1 million to $4 million in San Diego. Houston typically prices closer to the Fort Worth end of that range while offering demand drivers more comparable to the coastal markets.

What that pricing gap means in practice is straightforward. Institutional buyers are getting Long Beach demand fundamentals at Fort Worth pricing, in a metro where they can actually develop new supply. The arbitrage is hard to ignore.

The question facing every IOS operator on the Houston Ship Channel right now is not whether institutional capital will arrive. It already has. The question is how much of the cap rate spread will compress before the window closes.

Currently, IOS trades at roughly 6.0% to 7.0% cap rates, versus 5.0% to 5.75% for best-in-class traditional warehouse. Northmarq's IOS guide and CBRE's Outside Chance podcast both characterize the spread as 100 to 150 basis points in IOS's favor today, and both expect it to compress to 50 to 75 basis points as the asset class fully institutionalizes. American Realty Advisors describes IOS as "early entry into an asset class with all the drivers of industrial but a fraction of the capital costs."

At Ameritank, we operate a 42-acre Industrial Outdoor Storage yard in La Porte, Texas, located 2.4 miles from Highway 225 and Beltway 8. The site sits inside the same demand profile that institutional capital is buying everywhere else in the country — except we are operating it from the ground level, with direct visibility into the tenant base, the lease velocity, and the capacity constraints that the institutional buyers are still trying to underwrite from spreadsheets in New York and Philadelphia.

Three things are clear from inside this market. First, the petrochemical buildout is the demand floor. ExxonMobil's Baytown reconfiguration alone will require thousands of staging acres for contractor fleets and project laydown. Enterprise Products' NGL expansion adds more. The Permian-to-Houston frac sand corridor adds more still. None of this demand depends on macroeconomic conditions. It depends on commodity flows that are already underway and contractor schedules that are already booked.

Second, the truck parking crisis is the demand floor on the trucking side. Hours of Service is federal law. The 11-hour driving limit does not negotiate with vacancy rates. Fleets that need guaranteed nightly parking will pay for it, and the gap between 313,000 national truck parking spaces and the actual demand from 3.5 million U.S. truck drivers is not closing in any reasonable timeframe.

Third, the next wave of supply will come from Chambers County, the Highway 99 corridor, and Mont Belvieu — not from new development inside the established Ship Channel corridor. By the time that supply comes online, institutional buyers will have already absorbed the existing inventory in La Porte, Pasadena, Baytown, and Channelview at progressively tighter cap rates. The window for operator-level pricing closes at the same speed as institutional capital deployment, which is to say, fast.

Industrial Outdoor Storage is no longer an alternative asset class. Brookfield's $1.2 billion Peakstone deal in February 2026 was the closing argument. Alterra's $925 million Fund III, Zenith and JPMorgan's $1.5 billion joint venture, and JPMREIT's direct $95 million acquisition are all evidence of the same thesis: institutional capital has decided that IOS is core industrial real estate, and it is moving quickly to assemble the holdings before the cap rate spread closes.

What makes the Houston Ship Channel the most asymmetric play in the asset class is not just one variable. It is the combination of all of them at once. National-tier port volumes (4.3 million TEUs in 2025). The largest petrochemical complex in the country. Active expansion at ExxonMobil, Enterprise, and the Project 11 channel itself. The Permian-to-Gulf Coast frac sand corridor. A federal Hours of Service mandate that makes truck parking demand non-discretionary. And the only major U.S. zoning environment where new IOS supply is still legally and politically possible to develop.

The math is straightforward. National IOS vacancy at 2.5%. Rent premium of 17.9% over traditional industrial. Rent growth of 123% since 2020. A $214 billion addressable market, $3 billion in fresh capital deployed in a single quarter, and only five large industrial tracts left along the Ship Channel before development pushes northeast into Chambers County.

Every institutional IOS aggregator in the country has Houston in their top three target markets. Every other top metro has just made it functionally impossible to build new supply. The Houston Ship Channel is the asymmetric play because the demand is national-tier and the supply curve is still elastic. The window is open. It will not stay open forever.

Ameritank operates a 42-acre Industrial Outdoor Storage yard in La Porte, Texas, 2.4 miles from Highway 225 and Beltway 8 — providing truck parking, trailer staging, container storage, equipment yards, and frac sand staging at the heart of the Houston Ship Channel petrochemical corridor. Connect with the Ameritank team.

Andrew Viera

Business Development Executive, Ameritank

Andrew manages offtaker relationships, capital partnerships, and strategic positioning for Ameritank's 147-acre terminal on the Houston Ship Channel. He works across terminal development, investor relations, and market analysis to connect infrastructure capacity with commodity demand across the Gulf Coast energy corridor.