Fewer than five large rail-served tracts remain near the Houston Ship Channel. Land prices have tripled to over $1M per acre. IOS vacancy sits at 3.4% with 83% five-year rent growth. This analysis covers the rail infrastructure, unit train economics, construction costs, operator landscape, and regulatory requirements that terminal operators and industrial investors need to evaluate.

Rail-served industrial land on the Houston Ship Channel has become one of the scarcest and most valuable asset classes in U.S. industrial real estate. Fewer than five large tracts remain available near the channel corridor. Land prices have tripled in under a decade to over $300,000 per acre. IOS vacancy in Houston sits at 3.4%. And chemical rail carloadings hit an all-time record in 2025.

For terminal operators, logistics companies, and investors evaluating rail-connected properties along the Gulf Coast, the convergence of record petrochemical production, constrained land supply, and billions in new railroad capital investment is reshaping the competitive landscape. This report provides the hard data — car counts, construction costs, lease rates, throughput metrics, and regulatory requirements — that inform real decisions.

The Houston Ship Channel corridor is served by Union Pacific, BNSF Railway, and CPKC — all three connecting through the Port Terminal Railroad Association (PTRA), the terminal switching railroad founded in 1924 that operates 154–185 miles of track on both the north and south sides of the channel.

PTRA handles approximately 50,000–52,000 railcars per month across 226 industrial customers from 7 serving yards, including Pasadena Yard, North Yard, Manchester Yard, and South Shore. The railroad maintains capacity for 5,000 railcars at any given time with roughly 975 engine starts per month.

PTRA's commodity mix skews heavily toward petrochemicals: chemicals account for 28% of volume, plastics 22%, and coke 12%, with grain, steel, food products, and intermodal rounding out the balance.

Union Pacific provides direct Class I service in La Porte — including unit train capability at the Ameritank terminal site — while BNSF operates intermodal facilities south and north of the channel. The Houston Belt & Terminal Railway, jointly owned by BNSF and UP since 1905, provides additional interchange capability via its Magnolia Branch extending to Ship Channel industries.

Chemical carloadings hit an all-time weekly high of 33,745 carloads per week in April 2025, with full-year 2024 chemical carloads reaching a record 1.69 million — up 4.1% year-over-year, driven partly by low natural gas feedstock costs that give Gulf Coast producers a structural advantage. The AAR reported 14.06 million intermodal units in 2025, the second-highest tally on record.

Union Pacific committed $3.4 billion in capital expenditure for both 2024 and 2025, with $3.3 billion planned for 2026. The most significant Houston-area project is the Mainline Texas Industrial Park in Rosenberg, announced December 2025: a 2,000-acre master-planned development with 1,300 rail-served acres, 1,700 railcar storage spots, and potential for over 20 million square feet of Class A industrial development.

UP also launched on-dock intermodal service at Port Houston's Barbours Cut Container Terminal in 2023, expanding from 5 to 11 inland market destinations by March 2024.

BNSF's 2025 capital plan totals $3.8 billion, including $535 million specifically for expansion and efficiency projects. Key Houston-area moves include the North Houston Logistics Center in Cleveland, Texas (1,200 acres, opened September 2025) and expedited three-day LA-to-Houston intermodal service launched July 2025.

BNSF's Southern Transcon — the 2,200-mile corridor carrying 70% of BNSF's intermodal volume — is now 99.98% double, triple, or quadruple-tracked. BNSF reported that its customers invested a combined $5.3 billion in 2025 on rail-served facility projects, the highest rate in six years.

The TGS Cedar Port Industrial Park in Baytown — the largest rail-and-barge-served industrial park in the United States at 15,000 acres — completed a 900-railcar expansion in 2024 and interchanged more than 100,000 railcars for 50+ customers. The largest rail-served industrial lease of 2025 was a 496,421-square-foot deal at Cedar Port with Constellation Beverage.

For operators evaluating the economics of new rail connections, construction costs are the threshold question. Current estimates for rail spur construction on the Gulf Coast range from $300 to $400+ per linear foot for a straightforward single-track spur, or $2 million to $5 million per mile when including comprehensive site work, grading, drainage, and signal integration.

Turnout switches — the single most expensive discrete component — run $133,000 for a #10 turnout (the minimum grade for industry tracks), $155,000 for a #15, and $282,000 for a #20. A typical project connecting to a Class I mainline requires at least one mainline turnout, pushing baseline connection costs above $150,000 before a single foot of new track is laid.

Union Pacific's five-phase process for developing a rail-served facility includes initiation, project review, engineering, agreement execution, and construction. Engineering fees alone range from $18,000 to $170,000+. A straightforward spur takes 6–18 months; complex projects requiring environmental review or mainline modifications extend to 12–36+ months.

A critical nuance that sophisticated operators understand: rail spurs do not require Surface Transportation Board approval for construction. Under the ICCTA, spur and side track construction is federally preempted from state and local zoning interference. The STB issued a landmark Notice of Proposed Rulemaking in March 2026 proposing to reduce the prefiling notice period from 6 months to 45 days and expand categorical exclusions — a potentially significant timeline compression for new rail infrastructure.

Rail-connected industrial sites command a 15–30% premium over comparable non-rail properties, with the premium reaching the higher end in petrochemical corridors where rail is operationally critical.

Unit train economics remain the core value proposition for high-volume commodity terminals. A standard crude oil unit train consists of 100–120 DOT-117 tank cars, each carrying approximately 600–700 barrels, for a total train capacity of 70,000–85,000 barrels — the equivalent of 500+ truckloads in a single movement.

The modal cost comparison for Gulf Coast operations: pipeline runs $2–$5 per barrel for domestic long-haul; rail costs $10–$15 per barrel for long-haul and $3–$12 for shorter movements; truck runs roughly $215 per net ton versus rail's $70 per net ton on comparable lanes — a 3:1 cost disadvantage for truck.

BNSF's facility design guidelines specify a minimum of 6,900 feet of clear track (7,500 feet recommended) for liquid unit trains accommodating 96 tank cars, 2 buffer cars, and 4 locomotives. Loop track configurations — requiring roughly 3+ kilometers of track — allow continuous loading and unloading without uncoupling, achieving 2–4x the throughput of equivalent manifest-served terminals by eliminating classification yard dwell time.

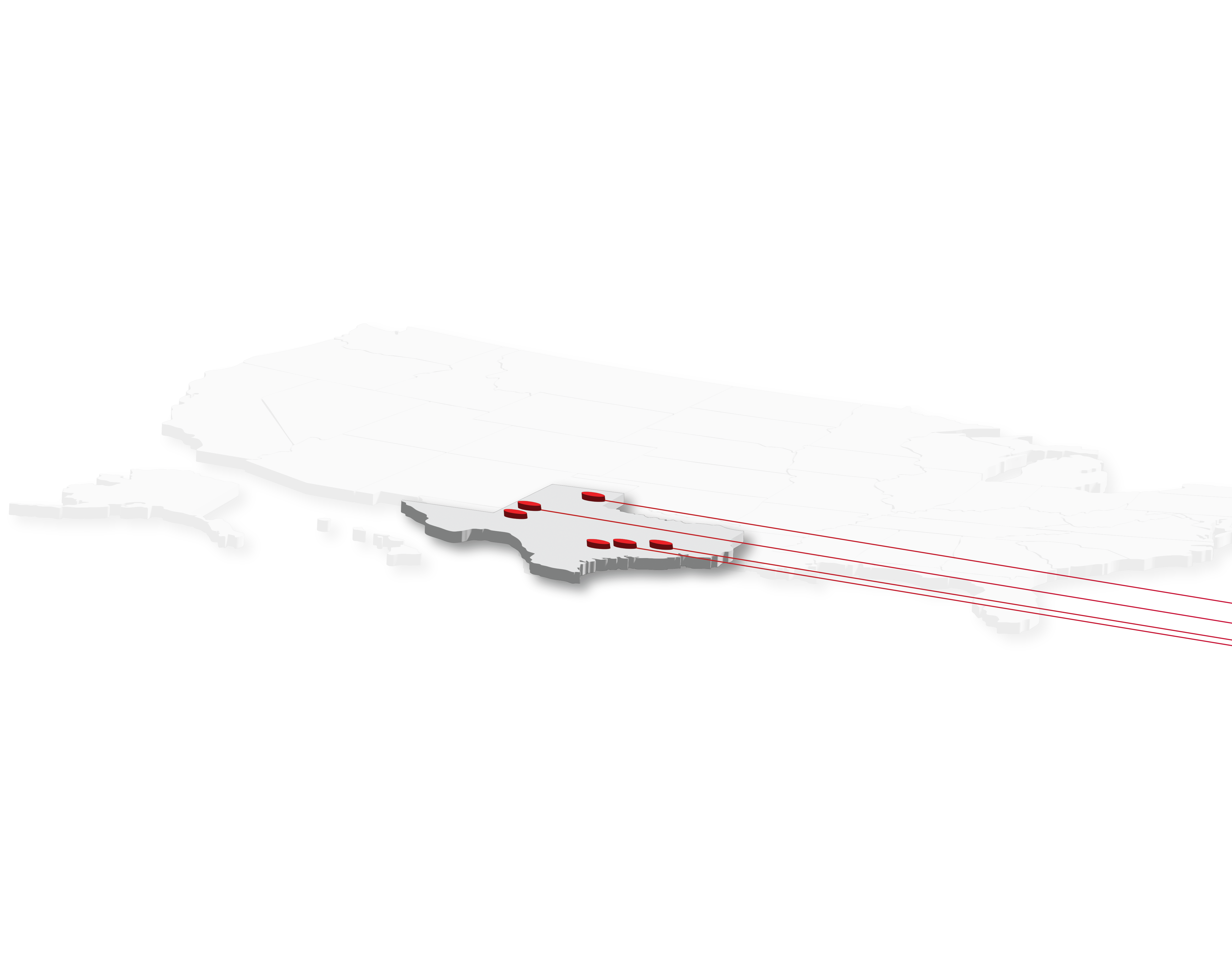

The scarcity of rail-served industrial land near the Houston Ship Channel defines the investment landscape. Only approximately 5 large industrial tracts remain near the channel, and that assessment predates several years of continued absorption.

Land costs in the southeast Houston market have nearly tripled in roughly eight years: developers report paying over $7 per square foot (approximately $305,000 per acre) for build-to-suit land near the Ship Channel, compared to $2–$2.50 per square foot eight years earlier. Manufacturing space vacancy across Houston stands at an extraordinarily tight 2.2%, with industrial rents at a record $10.67 per square foot NNN annually in Q4 2025.

The southeast submarket — encompassing the Ship Channel corridor through Pasadena, La Porte, Deer Park, and Baytown — led Houston in absorption during Q3 2025 at 1.4 million square feet. Industrial investment sales in Q3 2025 totaled $246 million across 298 properties at an average $94 per square foot and a 5.1% cap rate.

Over $50 billion in private-sector petrochemical investments are underway along the channel. Houston accounts for 44% of U.S. petrochemical manufacturing capacity https://houston.org/news/houston-continues-grow-world-class-manufacturing-powerhouse/ and is home to the largest petrochemical complex in the Western Hemisphere.

The market's response to Ship Channel scarcity is outward expansion. Union Pacific's 2,000-acre park in Rosenberg, BNSF's 1,200-acre logistics center in Cleveland, and Liberty Development Partners' 3,800-acre Gulf Inland Logistics Park near Dayton all represent the market correcting for channel land constraints.

Industrial outdoor storage has emerged as a breakout asset class nationally, and Houston's IOS market exemplifies the trend. Houston IOS rents average approximately $84,000 per usable acre annually with vacancy at just 3.4%. Houston's 5-year IOS rent growth of 82.8% dramatically outpaced bulk warehouse rent growth of just 10.7% over the same period.

Nationally, IOS rents have grown 123% since 2020, more than double the 58% growth in bulk warehouse rents. National IOS vacancy stood at 2.5% per CBRE's Q4 2025 report, versus 6.7% for traditional industrial.

Institutional capital flow into IOS has accelerated sharply: $1.7 billion raised by IOS investors in 2024, over $900 million committed in 2025, and marquee transactions including Peakstone Realty Trust's $490 million acquisition of Alterra IOS's 51-property portfolio. The NCREIF Expanded National Property Index shows IOS 5-year annualized returns exceeding the broader industrial sector by 126 basis points.

IOS cap rates run 50–150 basis points above standard industrial, though prime rail- and port-adjacent IOS in constrained markets trades at the compressed end of that spread. Typical IOS lease structures feature 5–7-year terms, NNN, with 3–5% annual escalators.

Ameritank's 147-acre facility in La Porte offers secured industrial outdoor storage with Union Pacific rail, deepwater barge dock, and direct Houston Ship Channel access.

Kinder Morgan operates the most significant rail terminal cluster on the channel, anchored by the Deer Park Rail Terminal — a 75-acre facility handling 12,000–15,000 railcars per month with 750 spots for railcar storage and direct pipeline connections to Shell Deer Park Refinery. Across five interconnected Houston Ship Channel terminals, Kinder Morgan controls combined storage exceeding 40 million barrels.

Cando Rail & Terminals completed its acquisition of the former TexasDeepwater Partners terminal in Channelview in December 2024 — Cando's first U.S. terminal operation. The facility currently offers 900 railcar spots with connections to BNSF, CPKC, and Union Pacific via PTRA. The full development potential of the underlying 988-acre site includes up to 12 million barrels of liquids storage.

Enterprise Products is expanding LPG export capacity by 300,000 barrels per day at its Houston Ship Channel Export Terminal, targeting service by end of 2026. While primarily pipeline-fed from Mont Belvieu, Enterprise's EHT complex operates 18 ship docks, 8 barge docks, and access to approximately 125 pipelines.

Howard Energy Partners operates significant Gulf Coast rail terminals at Port Arthur (450 acres, 1.35 million barrels, 8.8 miles of rail handling 5 unit trains simultaneously) and Corpus Christi.

The DOT-111 tank car phase-out for crude oil and ethanol was completed by May 1, 2025, with jacketed DOT-111s carrying Packing Group II and III flammable liquids remaining in service until May 1, 2029. All new crude-by-rail and chemical-by-rail tank cars must meet DOT-117J specifications : 9/16-inch minimum shell thickness, metal jacket with thermal protection, top fittings protection, and high-capacity pressure relief valves. Retrofit costs run approximately $43,500 per car for non-jacketed DOT-111s.

High-Hazard Flammable Trains — defined as trains with 20 or more loaded Class 3 flammable liquid tank cars in a continuous block or 35 or more throughout the consist — are subject to 50 mph speed limits, mandatory two-way end-of-train devices, and enhanced routing analysis.

PHMSA's real-time train consist information rule (finalized June 2024) requires railroads to push electronic hazmat consist data to first responders upon incident. Class I compliance was extended to June 24, 2026.

For terminal track, FRA's 49 CFR Part 213 permits designation of internal track as "excepted track" with a 10 mph speed limit and a maximum of 5 placarded hazmat cars per train. TCEQ air permitting in the Houston nonattainment area requires vapor recovery for loading and unloading operations.

Rail-connected terminals on the Houston Ship Channel require 3–10 MW of connected electrical load for a mid-size crude or chemical facility, with power consumption dominated by transfer pumps (40–60% of total load), steam generation for heating viscous products (15–25%), and vapor recovery systems (5–10%).

ERCOT wholesale electricity averaged approximately $26/MWh in 2024, down 46% from $48/MWh in 2023. Industrial customers in the Ship Channel area negotiate retail rates of 6–10 cents per kWh on medium-term contracts. However, ERCOT's inherent price volatility — wholesale prices spiked above $9,000/MWh during Winter Storm Uri — requires active risk management.

ERCOT's new Large Load Interconnection process requires formal study applications for loads exceeding 75 MW, but most rail terminals fall well below this threshold. Proximity to existing industrial substations along the Ship Channel materially reduces interconnection costs and timelines.

Ameritank's La Porte facility sits on 840 MW of existing power capacity — a legacy advantage from the site's former power plant operations that eliminates the power infrastructure bottleneck entirely for prospective terminal operators.

The Houston Ship Channel's rail infrastructure story is one of structural scarcity meeting unprecedented capital investment and commodity demand. PTRA handles over 50,000 railcars monthly across a network that hasn't materially expanded in decades. UP and BNSF are deploying over $7 billion annually in system-wide capital. Chemical carloadings are at record highs.

The operators who will capture the most value are those with existing rail connections in the channel's core — La Porte, Deer Park, Pasadena, Galena Park — where replacement cost exceeds $300,000 per acre and new supply is functionally impossible. Unit train capability transforms terminal economics by delivering 70,000–85,000 barrels per movement at one-third the per-ton cost of trucking. And as IOS vacancy holds below 4% with five-year rent growth approaching 83%, the optionality embedded in rail-connected outdoor storage acreage on the Ship Channel represents one of the more compelling positions in Gulf Coast industrial real estate.

The March 2026 STB permitting reform proposal, if finalized, could accelerate the next wave of rail infrastructure development — but for sites already connected, the moat is only deepening.

Andrew Viera

Business Development Executive, Ameritank

Andrew manages offtaker relationships, capital partnerships, and strategic positioning for Ameritank's 147-acre terminal on the Houston Ship Channel. He works across terminal development, investor relations, and market analysis to connect infrastructure capacity with commodity demand across the Gulf Coast energy corridor.